If that’s the case, use this calculator observe simply how much you will need to provides arranged since the a downpayment doing the home pick. Which calculator tend to imagine your own full settlement costs also the needed upfront Home loan Premium (MIP). You can make use of it calculator to find the restriction FHA home loan maximum to have a certain pick, yet not to determine this new maximium matter for your county and number you should use brand new HUD web site to discover local limits. Shortly after deciding regional constraints you can use the new less than calculator in order to figure your payments.

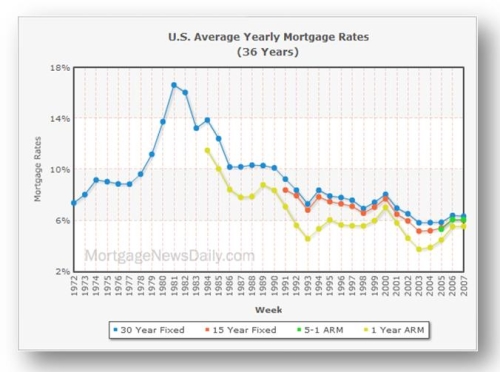

Latest Local 30-Yr Fixed Financial Costs

Another desk shows most recent regional home loan costs. Automatically 30-season get finance is actually showed. Simply clicking the fresh refinance option changes finance to refinance. Most other mortgage adjustment choice together with rates, down payment, home venue, credit score, label & Arm options are designed for options from the strain area in the the top of the new desk.

A basic Self-help guide to FHA Fund

To shop for a home try a difficult fling, particularly when you will be still building income. You can also have trouble with a decreased credit score and insufficient money to own downpayment. Instance is the situation with first-day homebuyers who have a tough time being qualified to have a traditional conventional mortgage.

But do not be concerned. You will find mortgage programs giving low-down payment choice and you may informal credit criteria. Despite a decreased credit rating, you can still pay for a property. One of these loan applications try backed by the newest You.S. Federal Construction Government (FHA).

Our very own publication usually talk about the maxims out of FHA funds as well as how you can use it on your side. We will contrast they that have old-fashioned mortgage loans and you can speak about their professionals and you will cons. From the knowledge your loan options, we hope this article helps you reach your homeownership specifications.

What are FHA Loans?

FHA loans are mortgages paid from the Government Houses Government (FHA). They guarantee mortgage loans given by FHA-backed simplycashadvance.net tax refund cash advance emergency loans 2022 online lenders such banking companies, mortgage people, and you will borrowing from the bank unions. FHA money are especially aimed toward low to moderate money individuals who want direction inside the getting property.

FHA funds was a popular financial support selection for earliest-go out homeowners and you will consumers having tight money. They show up having lenient borrowing conditions, low down money, and you will sensible settlement costs as compared to old-fashioned traditional mortgages. FHA fund can be removed as 30-12 months fixed mortgage loans, but they are plus for sale in fifteen-12 months and 20-year repaired-speed terms and conditions.

The brand new Government Homes Government (FHA) was oriented beneath the National Construction Work of 1934. It had been developed in a reaction to widespread foreclosures inside the High Despair. Doing 1933, ranging from forty% so you can fifty% off people defaulted on the mortgage. To relieve this problem, the newest FHA was created to raise funding circulates throughout the construction market.

Ahead of the High Depression, very lenders emerged while the adjustable-speed funds which have a finishing balloon percentage. Individuals can just only obtain fifty% to help you sixty% to finance a home. Mortgages had been generally planned with eleven to 12-season amortizing finance, that have been means less than just the present standard 29-12 months name. If for example the debtor could not spend the money for highest balloon commission, they leftover refinancing its financing to give the word. This program caused it to be difficult for consumers to afford houses, which fundamentally bring about big foreclosures.

Into the FHA set up, mortgages was basically covered for around 80% off a great house’s value, with a 20% deposit. It also written prolonged terminology and fixed prices giving good-sized time for consumers to expend their financing. Such structured lending strategies at some point enhanced the borrowed funds system. Because of the 1965, the latest FHA turned a portion of the You.S. Institution off Property and Urban Innovation (HUD).